Three Types of Aggregates

Standard Indices

Standard Indices

Pre-built indices using Credit Benchmark’s PD data and entity universe, segmented according to the CB industry schema. These are ready-to-use benchmarks for common market segments — US Corporates, European Financials, Global Technology, and more.Use these for benchmarking a portfolio against a published CB market view.

Custom Subscriber Indices

Custom Subscriber Indices

Indices built from Credit Benchmark’s PD data applied to your specific entity list. You define the universe and segmentation; we supply the Consensus PD data and run the aggregation.Use these when you want CB’s independent credit view on your own portfolio or peer group.

Contributor Bank Indices

Contributor Bank Indices

Indices built from your bank’s own internal PD data, aggregated using the CB methodology. Applies the same rigorous calculation process to your portfolio that powers CB’s standard indices.Use these for consistent time-series analysis of your internal book using a standardised aggregation approach.

Output Views

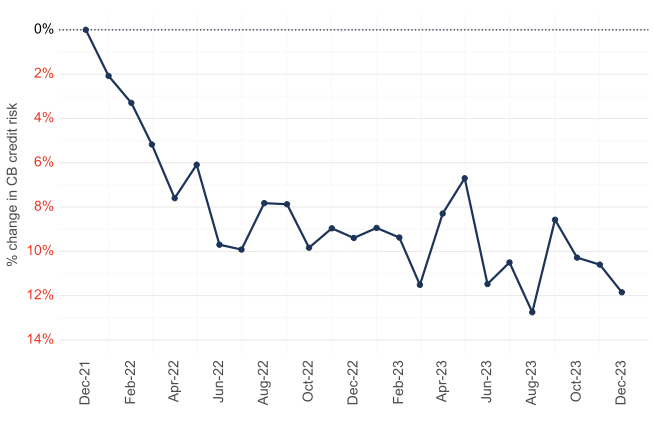

Each aggregate can be expressed three ways depending on the analysis:- Segment PD Average — absolute probability of default for the segment at each point in time

- Segment PD Rebased — relative change from a chosen base date, showing directional risk movement

- Segment Average Rating — aggregate PD mapped to the CB rating scale

Aggregate shown in rebased view